- CVV2 Basics: What It Is and Where It Lives

- What CVV2 Is Used For in Real-World Payments

- CVV2 vs. Other Security Layers You See at Checkout

- Is It Safe to Share Your CVV2 Security Code?

- What Merchants Should Do With CVV2 (and What They Must Not Do)

- Specific Examples: Safe vs. Unsafe Ways CVV2 Gets Requested

- How to Share CVV2 More Safely When You Must Use It

- What to Do If You Think Your CVV2 Was Exposed

- Why CVV2 Helps, but Does Not Solve, Card-Not-Present Fraud

- Quick FAQ: CVV2 Questions People Ask Most

- Conclusion

CVV2 appears during online and phone payments because the seller needs extra proof that you have the physical card. That is why people keep asking what is cvv2 security code, especially when they worry about scams and data leaks.

This guide explains what CVV2 checks, when it helps, and when you should refuse to share it. You will also get simple rules for safer checkout and clear steps to take if you think the code was exposed.

Quick answer: CVV2 is a three- or four-digit security code printed on your card that helps confirm you have the card during remote payments. It can be safe to share only when you control the channel, such as a checkout page you reached yourself or a call you initiated to a trusted business.

CVV2 Basics: What It Is and Where It Lives

1. What CVV2 Actually Proves

CVV2 is a card verification value used mainly in “card-not-present” payments. That means purchases where the card is not physically inserted, tapped, or swiped. Online shopping, paying in an app, and giving your card details over the phone all fall into that bucket.

CVV2 works as a lightweight check. It helps the merchant confirm you likely have the card in hand. It does not prove your identity by itself. Instead, it adds friction for thieves who only stole a card number from a receipt, a database, or a screenshot.

2. Where to Find CVV2 on Common Cards

Most cards print the code on the back near the signature strip. Some brands place it on the front. Either way, the goal stays the same: you must look at the physical card to read it.

If a checkout page asks for “CVV,” “CVC,” “CID,” or “security code,” it usually means the same kind of code. Brands use different names, but the purpose stays consistent.

CVV2 vs CVV vs CVC vs CID Mini-Explainer

Different brands and payment forms use different labels. Many forms say CVV, CVC, CID, or “security code.” In most cases, they all mean the same idea: a short code printed on the card that the seller asks for during remote payments. The key point is not the label. The key point is the channel. A legitimate checkout you reached yourself is very different from a link in a text message.

3. What CVV2 Is Not

CVV2 is not your PIN. A PIN is for debit ATM withdrawals and some in-person debit purchases. CVV2 also is not the card number, not the chip, and not a one-time password.

Because CVV2 is static, it can still be stolen. So, you should treat it like sensitive data, even though many legitimate merchants request it.

What CVV2 Is Used For in Real-World Payments

1. Online Checkout (Ecommerce)

At a normal ecommerce checkout, the merchant sends your card number, expiration date, amount, and CVV2 through a payment processor. The issuer then replies with an approval or decline.

Here is a practical example. You buy running shoes on a brand’s website. The site requests CVV2 because the card never touches a terminal. If a thief only has your card number, the CVV2 request can stop the transaction.

2. Phone Orders and Call Centers

Restaurants, travel agencies, medical offices, and small businesses sometimes take payments over the phone. In that case, the agent may ask for CVV2 as part of the standard card details.

However, you should slow down before you read it out. You want to confirm you called the official number or you trust the business. Scammers also run “payment verification” calls that sound professional.

3. Travel and Hospitality Holds

Hotels and car rentals often place a temporary hold for incidentals. They may ask for CVV2 when you book online, or when you provide card details in advance for a reservation.

Even so, policies differ. Some properties rely more on chip-present verification at check-in. Others want CVV2 to reduce remote booking fraud.

4. Why CVV2 Still Matters as Remote Payments Grow

Remote payments keep growing because people shop and pay bills online more often. In the United States, the Federal Reserve reported that 23% of consumer purchases and peer-to-peer payments were made remotely in 2024, which gives criminals more chances to attack card-not-present workflows.

As a result, merchants combine CVV2 checks with other tools, such as device signals, address checks, and bank risk scoring.

CVV2 vs. Other Security Layers You See at Checkout

1. CVV2 vs. Address Verification (AVS)

Many U.S. merchants use AVS, which checks the billing address you type against the issuer’s records. CVV2 checks a code printed on the card. AVS checks knowledge of billing details.

Used together, they reduce easy fraud. Still, neither one guarantees safety. A thief can steal both the address and the CVV2 in a single data leak.

2. CVV2 vs. Bank Alerts and Risk Engines

Banks also watch for unusual behavior. They look at merchant category, location, device patterns, and spending velocity. That is why a bank might decline a purchase even when you entered the correct CVV2.

From your side, this is good. It means CVV2 is only one piece of a larger decision.

3. CVV2 vs. Digital Wallet Tokens

When you pay with a major digital wallet, the merchant often receives a token instead of your real card number. Tokens reduce the value of stolen payment data, because criminals cannot easily reuse them elsewhere.

That is why many security teams prefer wallet payments for repeat purchases. You still should protect your wallet login, though, because account takeover can bypass the benefits of tokenization.

4. Why Fraud Keeps Happening Anyway

Criminals follow money. They target the easiest channel at the time. Global losses show the scale of the problem: the Nilson Report said payment card fraud losses worldwide dipped to $33.41 billion in 2024.

That context matters because it explains why merchants keep asking for CVV2. They do it because fraud pressure stays constant, even as tools improve.

Is It Safe to Share Your CVV2 Security Code?

Never share CVV2 through email, text, social media messages, or support chat logs. Also refuse any request for a photo of your card. If someone contacts you first and pressures you to “confirm” details, assume it is a scam and end the conversation.

1. The Practical Answer: “Sometimes, With Guardrails”

It can be safe to share CVV2 when you control the situation. For example, you type it into a legitimate merchant checkout on a secure connection. You can also share it with a trusted business by phone when you initiated the call.

It becomes unsafe when someone else controls the channel. Email and text messages are risky. Random inbound calls are risky. Social media DMs are risky. In those cases, a scammer can collect the full card details and spend immediately.

2. Red Flags That Mean “Do Not Share”

Refuse to share CVV2 if any of these apply:

- You did not start the conversation, and the person pressures you to “verify” a payment.

- The caller claims urgency, threatens fees, or tries to keep you on the line.

- The request arrives by email, SMS, or a messaging app link.

- The person asks for a photo of the front and back of your card.

- The person asks for one-time passcodes from your bank, too.

Those patterns often signal a social engineering attack. Scammers want speed, because speed beats your caution.

3. Why CVV2 Sharing Feels Confusing

People hear “never share your CVV,” yet checkout pages request it all the time. Both statements can be true, depending on context.

Think of CVV2 like a door key. You give it to a locksmith you called to open your door. You do not give it to a stranger who calls you and claims they work for the locksmith.

What Merchants Should Do With CVV2 (and What They Must Not Do)

1. Merchants Can Use CVV2 for Authorization Checks

Merchants collect CVV2 so the processor can pass it for authorization. That supports a match or mismatch response, which helps the merchant decide whether to ship goods or request extra verification.

This is why CVV2 often appears only on the payment step. It supports the moment of risk.

2. Merchants Must Not Store the Code After Approval

Merchants can use CVV2 for an authorization check, but they should not keep it after approval. Under Requirement 3.2, card verification codes are treated as sensitive authentication data that must not be stored after authorization. That is why a legitimate subscription system saves a token, not your CVV2.

This matters for subscriptions and “card on file” setups. A business can store a token or a reference to charge you again, but it should not keep CVV2 in its database.

3. What This Means for You as a Customer

If a site says, “We need your CVV2 to keep it on file,” treat that as a warning sign. A well-designed system does not require CVV2 for future recurring charges after the initial setup.

Also, if a merchant support agent asks you to email your CVV2 “for verification,” refuse. Instead, ask for a secure payment link, or call back using the number on the merchant’s official website.

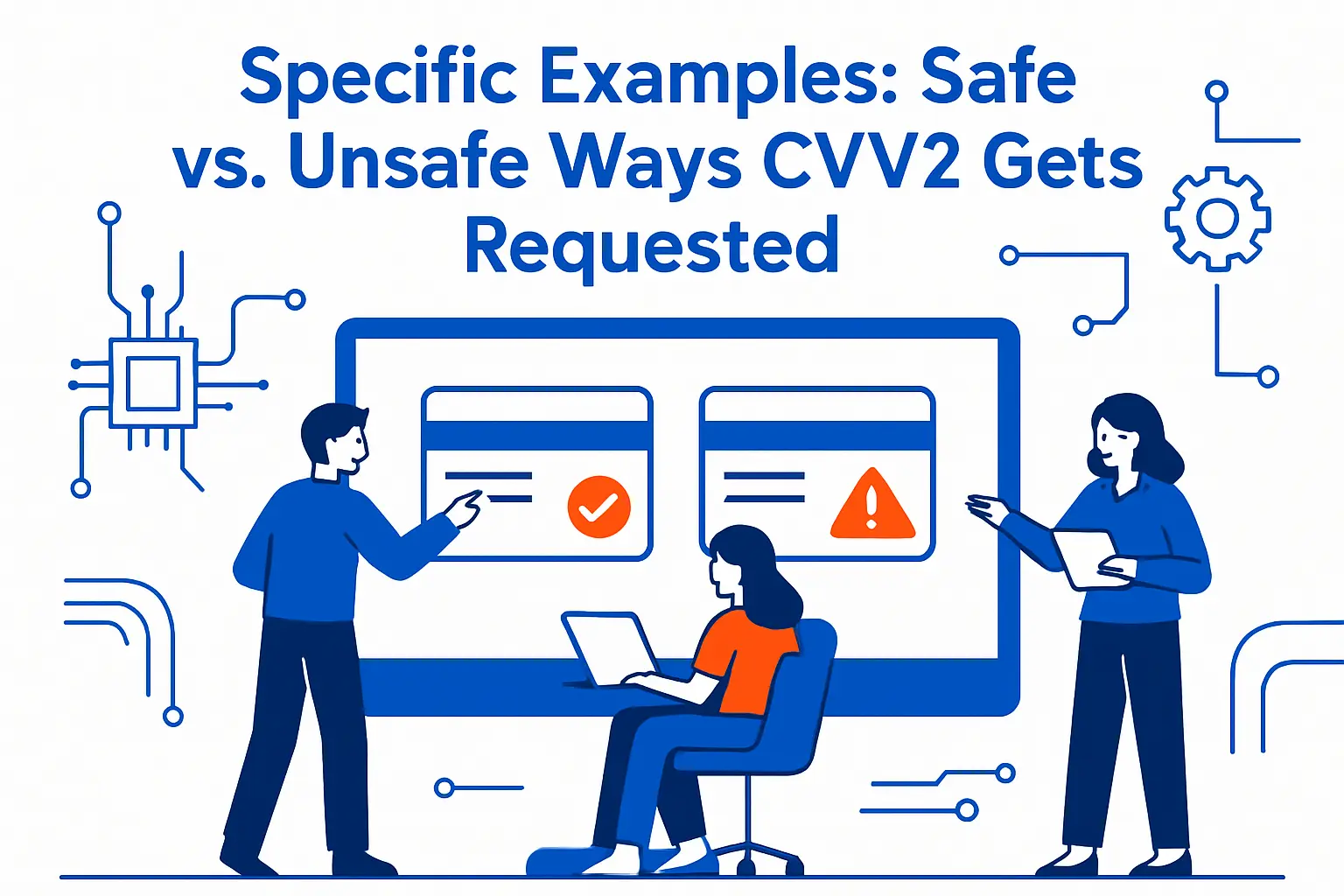

Specific Examples: Safe vs. Unsafe Ways CVV2 Gets Requested

1. Safe Example: You Type It into a Known Checkout

You navigate to a retailer by typing the URL yourself or using a saved bookmark. You add items to your cart. You see a normal payment page with clear branding, a lock icon, and standard payment fields.

In this case, typing CVV2 can be a reasonable risk. Still, use extra checks. Confirm the domain spelling. Avoid random coupon sites that redirect you to strange payment pages.

2. Safe Example: You Call the Merchant and Pay a Bill

You call your utility provider using the number printed on your bill. You choose the automated phone payment option or speak to a billing agent. You provide your card details, including CVV2.

This can be acceptable because you controlled the contact path. You reached the right business on purpose.

3. Unsafe Example: “Your Package Is Held” Text Message

You get a text that claims a delivery failed. The link goes to a page that asks for your full card details and CVV2 to pay a small “redelivery fee.”

This is a common pattern. The low fee lowers your guard. Then the attacker uses your data for larger purchases elsewhere.

4. Unsafe Example: A “Bank Security Team” Calls You

A caller claims your bank detected fraud. They say they must “confirm” your card number and CVV2 to stop it. That is a trap.

Banks may verify identity, but they do not need your CVV2 to protect you. End the call and dial the number on the back of your card.

How to Share CVV2 More Safely When You Must Use It

1. Use Stronger Payment Methods When Available

If a merchant supports a digital wallet, use it. If you can use a virtual card number from your issuer, use it. These options reduce the damage if the merchant’s systems get compromised later.

Also, prefer credit cards for online purchases when possible. Many cards provide stronger dispute paths for fraud, and they keep funds in your bank account untouched.

2. Reduce Exposure During Checkout

Small habits lower risk:

- Type the site address yourself instead of clicking ads when you feel unsure.

- Confirm the domain spelling before you pay.

- Avoid paying while connected to public Wi‑Fi for high-value purchases.

- Turn on transaction alerts so you spot misuse fast.

These steps do not replace CVV2. Instead, they strengthen the environment around it.

3. Protect Your Card Photos and Screenshots

Many modern leaks are self-inflicted. People store card photos in their camera roll “just in case.” Then they lose a phone or get their cloud account compromised.

Delete any card images you do not truly need. If you must store something for a one-time form, use a secure password manager that encrypts data. Better yet, do not store it at all.

What to Do If You Think Your CVV2 Was Exposed

1. Act Fast, Because Speed Limits Losses

If you entered your card details on a suspicious page, assume the attacker captured them. Start by locking the card in your banking app, if your bank offers that feature. Then call the issuer and explain what happened.

Next, review recent transactions and pending authorizations. Report any unauthorized charge immediately.

2. Replace the Card, Not Just the Password

CVV2 is tied to the physical card. You cannot “reset” it like a password. In most cases, the safest move is to replace the card number entirely.

After you replace the card, update any legitimate subscriptions. Watch for failed payments so you do not miss essential bills.

3. Watch for Follow-Up Scams

After a leak, scammers often try a second step. They might pose as the merchant, the bank, or even “fraud support” to collect more information.

Consumer fraud keeps rising, and the FTC reported that consumers lost $12.5 billion to fraud in 2024. So, treat unexpected “help” messages with skepticism, even if they reference your recent issue.

What to Send to Your Bank Checklist

- The exact site or message that asked for your card details

- The time you entered the information and whether you received any confirmation

- Any suspicious charges, even small ones that look like tests

- Whether you shared only the card number or also shared CVV2

Why CVV2 Helps, but Does Not Solve, Card-Not-Present Fraud

1. Criminals Often Steal CVV2 Along With Card Numbers

If attackers compromise an ecommerce database, they may steal card numbers but not CVV2, because merchants should not store it. That is one reason CVV2 still adds value.

However, many other theft methods capture everything at once. Phishing sites can collect the full set of details. Skimmers and hidden cameras can capture the back of a card. Insider theft can happen too.

2. Fraud Shifts Toward the Easiest Target

Fraud trends show that remote transactions remain a prime target. For example, in Europe, card-not-present fraud often dominates card loss categories. A FICO analysis citing UK Finance found that card-not-present fraud accounted for around 70% of total card fraud losses in that context.

The takeaway is simple. CVV2 is useful, yet fraud still moves through remote channels. That is why you should pair CVV2 caution with stronger habits, like verifying who you are paying.

3. The Best Defense Mixes Technology and Behavior

Security tools help, but your actions still matter. When you slow down, verify the merchant, and avoid risky channels, you cut off many attacks before they start.

Also, when you monitor alerts and statements, you shrink the time window criminals get to keep spending.

Quick FAQ: CVV2 Questions People Ask Most

1. Can a Legitimate Company Ask for CVV2?

Yes. Many legitimate merchants ask for it during a card-not-present payment. The key is how they ask and where you provide it. You want a secure checkout or a call you initiated.

2. Should You Give CVV2 to Customer Support in Chat?

Avoid it. Chat tools may store logs, and you cannot always confirm who has access. Ask for a secure payment link instead, or pay through the account portal you access directly.

3. Why Does a Subscription Site Ask for CVV2 Again?

Some sites ask for it when you change billing details or start a new purchase flow. That can be normal. Still, it should not ask you to send CVV2 by email, and it should not claim it will store the code for future charges.

4. If Someone Has My Card Number but Not CVV2, Am I Safe?

You are safer than if they had both, but you are not fully safe. Some fraud attempts do not require CVV2, and some merchants do not enforce the check. Treat any exposure of your card number as serious.

Conclusion

CVV2 adds a useful friction step, but it does not make remote payments risk-free. Treat it like sensitive data and share it only in controlled, verified situations. If anything feels rushed or unexpected, stop and switch channels by visiting the merchant site directly or calling the number on your card. That single habit prevents many of the most common CVV2 scams.